With a new financial year comes updates of economic forecasts. The Conversation, for instance, has just polled 27 forecasters for their GDP outlook for the next year: on average, they expect anaemic growth in real GDP of 1.5 percent, while half think there is at least a 50 percent chance Australia will go into recession. Should investors worry?

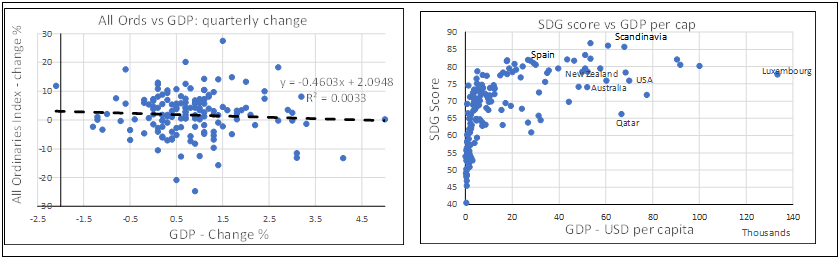

Let me answer the question in two parts. First, does GDP drive investor income? The chart at left plots quarterly values during 1985-2023 of change in the All Ordinaries Index against change in Australia’s GDP. The data are all over the place and there is obviously no reliable link between GDP and stock prices. This matches more detailed academic studies using decades of data and many countries. Although not shown, a similar plot of average capital city house price change against GDP shows no meaningful link either.

No doubt workers and consumers benefit from economic growth, but change in GDP does not necessarily affect investor income.

This leads to the second part of my answer which looks at the impact of GDP on wealth. Savers with a long-term view will have goals built around enjoyment of their nest egg, by self or family. An important part of accumulating wealth, then, is ensuring an attractive future environment and society. The latter is uncertain given that post 1970s capitalism has laid waste to a quarter of the economy – including crop and animal production, finance, food and beverage manufacturing, pharmaceuticals and health services, and information technologies – which have halved the number of wild animals and fish, triggered epidemics of obesity and mental illness, clogged infrastructure, and brought poor governance, along with chronic consumer scams and financial crises.

Such concerns encourage strategy that promotes national wellbeing, and led the United Nations to develop 17 Sustainable Development Goals (SDG), which cover human well-being, ecosystem resilience, industry and governance. Data are available in a standardised format for all countries at the UN’s SDG Database and are plotted in the right chart against GDP per capita from the World Bank database.

This second plot shows that broad-based national wellbeing rises with GDP per capita up to about $US60,000 per year – which is around Australia’s value – and then declines. Scandinavian countries enjoy highest well-being, while anglophone countries – including Australia – enjoy significantly lower standard of well-being despite high GDP per capita.

Why is GDP of doubtful value despite its typically depicted role as “a comprehensive scorecard of a given country’s economic health” or similar. In reality, it only counts priced goods and services, and so ignores free goods such as unpaid work, leisure, Wiki and ABS statistics. GDP is also poor at counting quality, and so cannot distinguish good health care or education from bad. It is also blind to loss of wealth: thus natural disasters are GDP-positive through the rescue operations and rebuilding they trigger; as is demolishing a perfectly good home to build a McMansion.

People actually have lower GDP per capita when they live in a country that is healthy, has fewer natural and industrial disasters, and uses resources efficiently.

In short, GDP (and other outdated performance objectives such as profit) provide little guidance for investors, and promote unsustainable environmental, social and economic outcomes because they relate only to the quantum of economic activity and do not consider its quality.