I am not geeky enough to read financial statements for entertainment, but it can be instructive because they are what company management wants the world to hear. This article listens to Tesla Inc, which is the world’s eighth largest company by market capitalisation and whose CEO is the world’s richest person.

To set the scene, Tesla CEO Elon Musk was a founder of what became PayPal, and in 2004 became the largest shareholder in newly formed Tesla. Since 2019 Tesla has been profitable, and in 2022 delivered 1.3 million vehicles, which made it the world’s eighth largest manufacturer of motor vehicles.

This analysis draws from Tesla’s 2022 annual report (10-K filing with the US SEC) and 2023 proxy statement. I have several take-aways.

First, is the company taking the mickey? Filings report the position of Elon Musk as Technoking of Tesla and Chief Executive Officer; and of Zachary Kirkhorn as Master of Coin and Chief Financial Officer. A Google search shows no other company that uses these titles, so they potentially reinforce the impression that Musk/Tesla do not play by the rules. The last is based on multiple fraud-related enquiries by the SEC and FBI and a string of critical press reports (examples here and here), and the current Department of Justice investigation into claims by Tesla of its vehicles’ range and self-driving capability. This also has echoes of the hubris that preceded implosion of bubbles as diverse as cryptocurrencies in 2022, emerging markets most recently in 2007, Enron in 2001 and Y2K-dot.com.

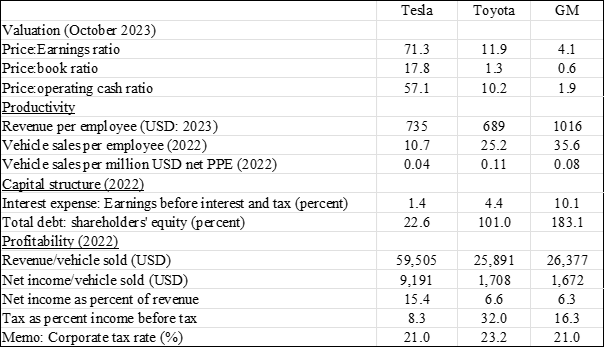

Other relevant points are made by the table which compares Tesla’s financials against those of the world’s largest carmaker Toyota and the largest US manufacturer General Motors. Data are from Yahoo finance, and are in US dollars for Tesla and GM and in Yen for Toyota.

My second take-away is that Tesla seems overvalued. It is selling at a price:earnings ratio of 71, which six times that of Toyota; and 18 times that of GM. Telsa’s worldwide vehicle sales are less than one tenth those of Toyota and GM combined, but – with its high P:E ratio – Tesla is valued at three times their combined market capitalisation. Perhaps more importantly, Tesla is selling at 17.8 times shareholders’ equity (i.e. book value of assets minus liabilities), whereas GM and Toyota sell at 0.6-1.3 times; and is selling at an even higher ratio of price to operating cash flow.

Third is Tesla’s relatively low productivity. Each year it sells about 11 vehicles per employee, which is well below GM’s 36 vehicles per employee and Toyota’s 25. Also, for every million dollars of plant, Tesla sells 0.04 vehicles, whereas Toyota and GM sell two to three times more.

As a positive, Tesla’s capital structure is conservative. Its debt is less than a quarter of shareholders’ equity whereas gearing is higher for Toyota and GM; and its interest expense of one percent of earnings before interest and tax is well below that of Toyota and GM. Tesla’s financial position has improved in the last few years and in 2022 its S&P credit rating was lifted from junk grade to BBB. For comparison, Toyota is rated A+ and GM at BBB.

The magic in Tesla’s financials comes from the high profitability built into its business model. Almost 90 percent of Tesla’s revenue comes from its automotive segment, and average revenue per vehicle sold is nearly $60,000, which is more than twice that of Toyota and GM. Tesla makes a profit of over $9,000 on each vehicle, whereas it is less than $2,000 for Toyota and GM.

A caution in the reported accounting profitability is that Tesla reports tax paid that is 8.3 percent of income before tax, which is well below the statutory US corporate tax rate of 21 percent. Less than half of Tesla’s reported profit is taxable. By contrast taxes paid by Toyota and GM are much closer to the statutory rate. Tesla offers a reconciliation of the difference in its Annual Report (page 82) which attributes the gap mostly to ‘Change in valuation allowance’, ‘Foreign income rate differential’ and ‘Excess tax benefits related to stock based compensation’.

An imponderable is the fragility of Tesla’s margins. Letters from CEO Musk have stated Tesla’s mission is to develop “mass market electric cars” and that it will not initiate patent lawsuits to protect its technology. China has embraced this opportunity and is set the swamp the global market with cheap, quality EVs. And the global market relies on government subsidies that are as high as USD7500 in the United States, USD11,500 in Singapore and USD20,000 in Norway.

So what does all this conclude? The Wall Street Journal markets section reports that 45 analysts follow Tesla and that 19 (42 percent) have a buy or overweight recommendation. By contrast 56 percent of analysts following GM say buy; and 70 percent of those following Toyota say buy or overweight.

To conclude, according to conventional criteria, Tesla is overvalued by a factor of up to ten or more. This cannot be justified by its operations, which lag competitors in asset and labour productivity. Part of the explanation comes from Tesla’s marketing success, where its vehicles are priced at twice those of Toyota and GM, and give a profit margin that is 2.5 times that of competitors. Much of the justification for high share price is presumably that Tesla has unique high tech and entrepreneurial attributes. Musk supporters shrug off doubts, and are led by a Morgan Stanley projection of near doubling in its share price.